“A nation of shopkeepers Airbnbers” That’s what the government thinks!

BBC News on the 8th of 2024 covered the removal of Furnished Holiday Lets (FHL) tax benefits in the Spring budget, and we thought it was worth investigating what may happen and why.

As far back as 2022, the Office of Tax Simplification (OTS) produced a report summarising some options for reforming the taxation of letting properties for individuals. This included recommendations for changing or abolishing the special FHL rules. This Francis Clark article explains the proposed reforms in detail, which have now come to pass.

Move forward a few years, conveniently in an election year, and the reforms are being implemented. BBC News explained FHL briefly and highlighted the part of the Chancellor’s speech that this was aimed at solving the housing crisis. This was followed by interviews of Whitby people who admittedly said tourism was thriving, but housing shortages and prices prevented locals from buying.

This reform removes the current tax advantage for landlords who let short-term furnished holiday properties over those who let residential properties go to longer-term tenants.

This is the government webpage link for anyone who missed this announcement and is confused about the previous benefits. These benefits will be removed in April 2025 and they forecast recouping £300m.

In essence, the tax advantages allowed netting off costs such as

- Advertising or letting agency fees.

- Products bought for the property (cleaning products and welcome packs).

- Maintenance and cleaning costs.

- Insurance relevant to an FHL (e.g. public liability, buildings and contents insurance).

- Utility bills or refuse collection.

- Interest on loans associated with the property (the big one)

- Travel and subsistence (e.g. travelling to and from holiday let).

There are also serious considerations regarding capital gains, capital allowances, tax allowances, rollover relief, and many other tax nuances that experts must resolve (or not) for FHL owners. Again, Francis Clark does an excellent job of describing the impact, which could get very complicated! Consult your accountant.

NOTE: If you are a UK manager or owner, we suggest you subscribe to PASCUK.co.uk, which will keep all its members updated as these and other regulations evolve.

Will it Work?

The first question is, why have holiday rental properties increased in volume so much?

- Money was cheap, and returns on deposits were low.

- Dare I say the “Airbnb” effect, where a single platform, through excellent PR, alerted people with resources to short-term rent more quickly.

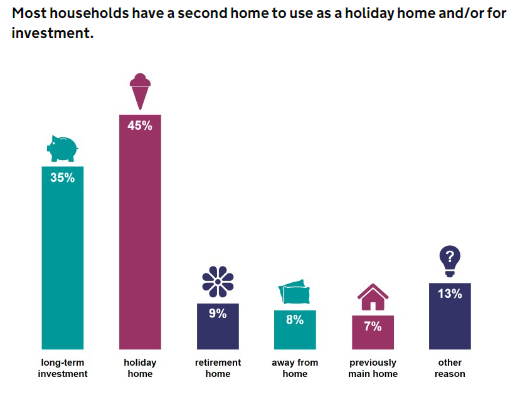

- Second homes offer a long-term bricks-and-mortar investment AND the opportunity to get away to the sea or countryside for some weeks of the year. There are plenty of reports that over 50% of people would like to live near the ocean, and higher numbers if you include the countryside, lakes, and rivers.

- There were tax advantages over residential letting, although there are claims related to upkeep that can be offset in residential lettings.

- Hotels are pricier pp/pn, and with a more mobile generation and baby boomer retirees on the horizon, second homes for partial yearly income made so much sense.

The Housing Argument

Apart from the treasury gaining more income from a few hundred thousand homes, the question is the Government’s argument that this has been done to level the playing field with home ownership, residential letting, and local affordability.

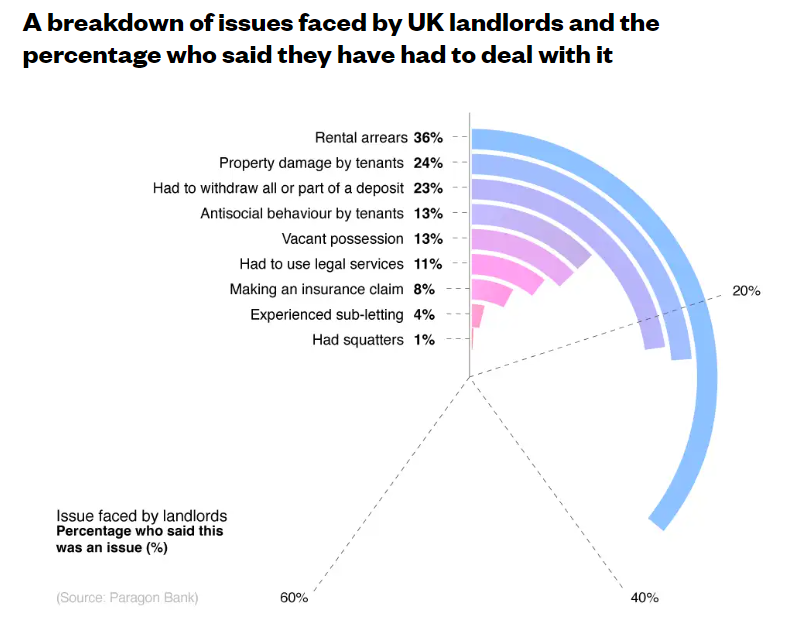

In the past, I have been both a residential landlord and STR property owner; the latter was much more favourable as not all tenants were great. STRs ensured the guest left the property in top condition, regularly maintained, and easy to sell. This graphic illustrates the worry of residential letting!

The government has also produced a Renters Reform Bill, meaning the tenant has greater rights over being evicted and multiple other challenges that part-time landlords may find unacceptable. This is a definite concern.

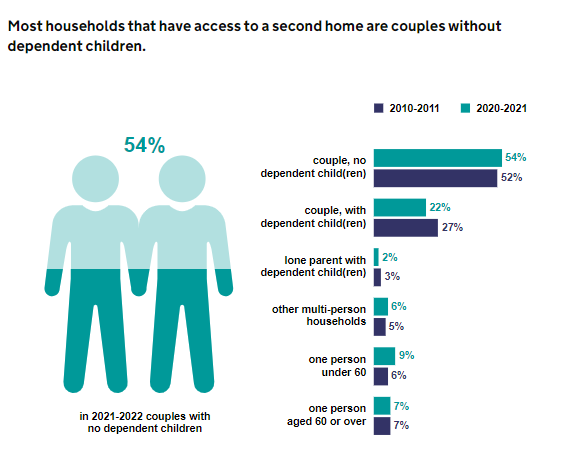

It is probably wise to look at the ownership demographics and distribution to understand what may happen:-

Why registration is a good idea!

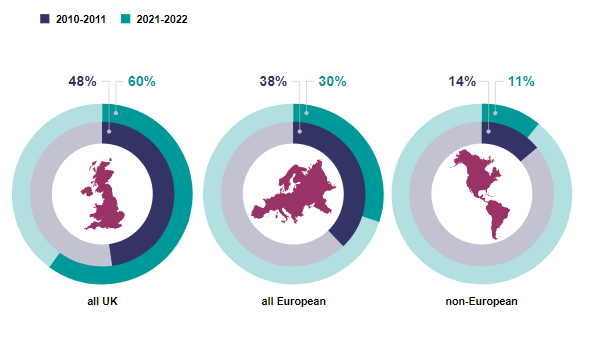

In 2021-22, 60% (482,000) of second homes were in the UK, and 40% (327,000) were outside the UK. These numbers are not split into private use, residential letting, or STR; however, data from the Department for Levelling Up, Housing & Communities (DLUHC) showed almost twice as many dwellings listed as empty as there are for second homes (468,000 vs. 253,000, respectively).

According to The Times, in 2016, there were about 83,000 Airbnb listings in Britain, of which about half were for entire properties. By 2019, the number had reached 257,000. We see reports of a 40% + increase since then, and the number of properties is closer to 500,000, of which 50% + are perhaps whole properties and would match those that are. Airbnb numbers are unreliable as the average incomes are low; thousands are not rented all year and have urban hotspots. These will not have reported incomes or be considered options for residential letting, no doubt.

Managers used to represent circa 50% of the full-time letting in the leisure industry, and we can see circa 125,000+ complete properties from professional managers being marketed, which would support these numbers. Major urban/city areas have much higher numbers, as seen above. We also now have tree houses, lodges and no end of alternative accommodation being booked.

According to AirDNA, the holiday rental market in the UK reached a new peak in August with 346,000 listings, of which 280,000 were entire properties (which validates the other data), including houses, cottages, apartments, treehouses and yurts. New regulations in Scotland have already caused a decrease in supply in areas such as Glasgow, Aberdeen, Argyll and Bute in Scotland, raising concerns of a supply drop similar to that which happened in Amsterdam, where listings fell by 64% from their previous high in August. The FHL change is not as dramatic but will have an effect.

Registration is a good idea to clarify and make sense of all the data. This should have been done before the government made essential decisions on ambiguous data.

These figures include overseas properties too, but the UK has seen an increase and, post-Brexit, a decrease in numbers abroad.

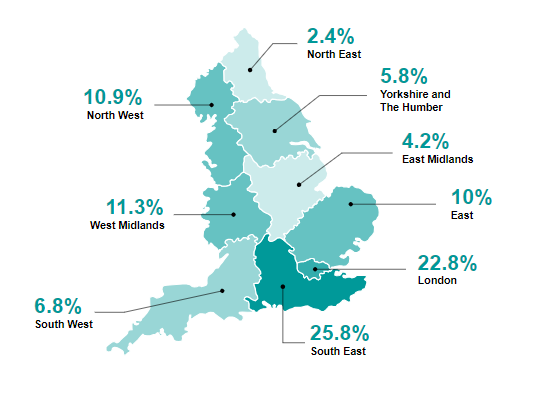

According to government data, the geographic location of these English homes is below! This is 2022.

Now, check the demographics of the ownership. Using the numbers above, the South West has circa 17,000 properties and is one area where MPs supported removing tax benefits.

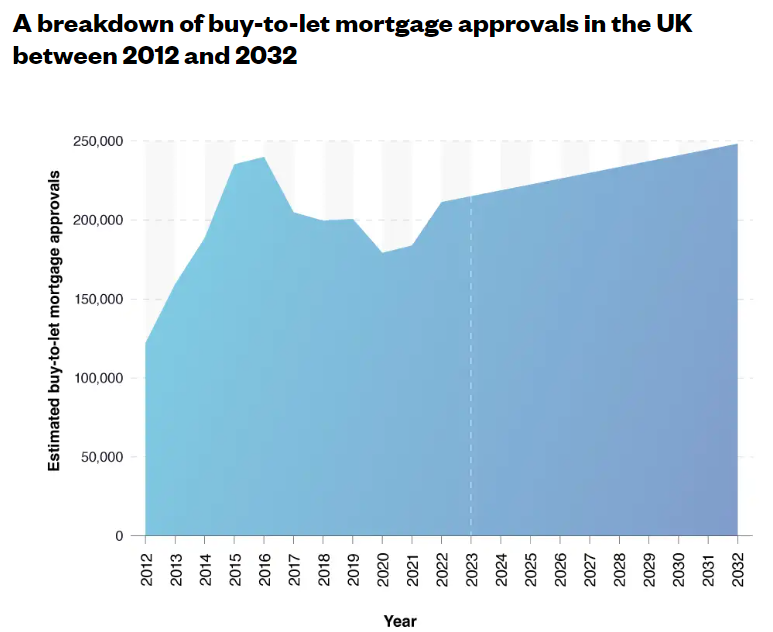

Mortgage issues

Interest payments not being netted off in the future is probably one of the most significant elements that will ensure a conservative government loses more votes among their usual followers.

The statistics for buy-to-let mortgages are revealing. Although this USwitch report covers all types of mortgages and rental businesses, it shows the increase over the years. We can expect a slowdown and even a drop-off now.

What does this financially mean to a second homeowner who rents out?

According to this company’s (IFA Mag) analysis, an owner could lose an average of £2,835 a year in tax. The calculations are based on a property purchase price of £350,000, with an annual mortgage rate of 4.5pc and £20,000 rental income. For owners of holiday lets, this could significantly reduce their net income. Should they lose the ability to deduct mortgage interest in full (in favour of a 20% deduction), alongside the potential increase in capital gains tax, this could make the holiday business less financially attractive.

The Government believes that it will recoup £300m from this. If this were the average per property/owner, then that would be 100,000 homes. Presumably, they expect the other 175,000 homes to be available for residential rent. We already have a backlog of 4.3m homes! This is just scratching the surface!

Real Analytical Research. We are not alone!

To add a little science to this, the Swiss have had similar problems, and this peer-reviewed paper did some significant research to identify the effect of second-home restrictions, with interesting outcomes.

Introduction

The paper explored the recent global phenomenon (2012 onward) of the surge of investment in ‘second homes’—properties that are not used as primary residences—and the subsequent political backlash against wealthy investors in such properties. Their main focus was on the impact of constraining second-home investments on residents and the value of their primary residences.

Back in 2016, the year of this paper,

Quote – in Switzerland alone, there are currently around 600,000 second homes – almost one such home for every five households. Yet, the investment boom in second homes is neither just a Swiss phenomenon nor confined to touristic countries. It is a worldwide phenomenon. Countries such as the United States, the United Kingdom, France, China, or Singapore have seen a dramatic increase in wealthy individuals investing in second homes in recent years.

Conclusion

Quote: Constraining new second-home investments hurts local homeowners via lower wages and *lower primary house prices. Renters benefit from lower rents but are not better off overall. This is because the rent fall is commensurate to a decrease in local wages.

*Note: The quoted decrease in house prices was up to 12%, keeping most starters out of the market.

Prediction for Leisure and some urban destinations

- Many owners will continue to consider their second homes as appreciating assets and try to raise rental prices to avoid loss of income, but they will be more concerned about “washing their face” than profit. Guests are already paying too much, and occupancy is “soft,” so tourism will suffer. House prices may drop 5-10% locally, affecting existing residences too.

- The FHL rules require stays of no longer than 30 days, so expect the more mobile traveller out of season and fewer turnarounds and expenses.

- Those close to retirement age may decide to sell their primary home, move to their second home earlier than planned and have cash! All the places the government wants to stop over-holiday renting are the most popular retirement destinations! We see this already: a higher percentage of people over 65 are moving. This government report shows that the population in rural areas has a higher proportion of older people than in urban areas. The average age in Rural areas is higher and has increased faster than in Urban areas.

- Some will residentially let, of course, but prices will be high initially and then be challenged as wages get hit as local gross income drops, especially in tourist areas.

- Leisure destinations tend to have properties in lovely places. Those that sell will not discount heavily, but more properties may be on the market. These will be picked up as early retirement properties and empty holiday homes or places for their children to live or subsidise for holidays.

- 90% of these destinations rely on tourism; without that, there is little employment except for local government and services. The government has clarified that there will be cuts, and local authorities are already cutting services. The complaint has always been ghost towns in the winter! Without affordable accommodations and sufficient choices, they may also be ghost towns in the summer. The European Southern sun is still attractive to travellers and often less expensive.

- Necessity is the mother of invention, and well-run rentals, which are, in effect, small businesses, will start to think outside the box and work around this new scheme in creative ways. Already, tax experts and entrepreneurs are considering ways to achieve this.

- There are already options, such as using a private limited company! This article explains the reasons and process, but it is not for everyone, and your accountant probably needs to be involved. This may be the only solution for those with multiple ownerships and full-time businesses.

- A limited number of hotels will win, raising prices. With the rise of the aparthotel trade, they will need the correct licenses. They will replace holiday cottages and make them unavailable for locals to rent! Global real estate corporations may own these and not reinvest locally.

Sad Victorian BnBs and guest houses, ready for conversion, are potentially cheaper alternatives to houses for local people to buy. Still, the construction industry is not doing well, and planning delays and constraints mean this will also face hurdles.

- The registration scheme will mean grandfathered-in properties that have been rented will see greater values, so there may be a rush to buy more holiday homes before June 2024, having the opposite effect on prices! We will see restrictions happen, but those who restrict the least may see the most tourism income.

A politically focused sticking plaster only?

Building more housing is the simple answer, and this FHL exercise seems just a politically guided, election-year sticking plaster. £300m is the expectation, probably enough to run the NHS for a day or so, depending on the time of year.

Then there is the fact, reiterated, that in 2022, Data from the Department for Levelling Up, Housing & Communities (DLUHC) showed almost twice as many dwellings listed as empty as there are for second homes (468,000 vs. 253,000, respectively).

Just saying.