If we thought that the turn of the century’s “Internet age” and the theoretical levelling of playing fields was a brave new world, then here we are again, but with lessons to learn from 20 years ago! Let’s not make the same mistakes! This journey offers a remarkable insight into how OTAs succeeded.

The opportunity lasted about five years before the well-funded US aggregation platforms descended on the industry, and many were not well prepared; some better than others, of course, and the divisive nature of the approaches fooled most, and as we see today, they are platform hostages. Yes, go on, say it’s what the Internet caused, but the Internet was the rails; the investors and the intent were the fuel and direction of plunder. No one can argue that, looking at the profitability of the behemoths, the extraction of income from local communities, the smart tax manoeuvres, and the company geographies. Let’s delve into some examples of how OTAs succeeded.

If you would like to watch Google’s LLM Notebook version of this article, it has done a decent job of interpreting it.

1. The Genesis of Digital Rentals:

Understanding the strategies that enabled OTAs to succeed will provide valuable insights for future industry developments. For a comprehensive understanding, we must explore the factors that contributed to OTAs’ success.

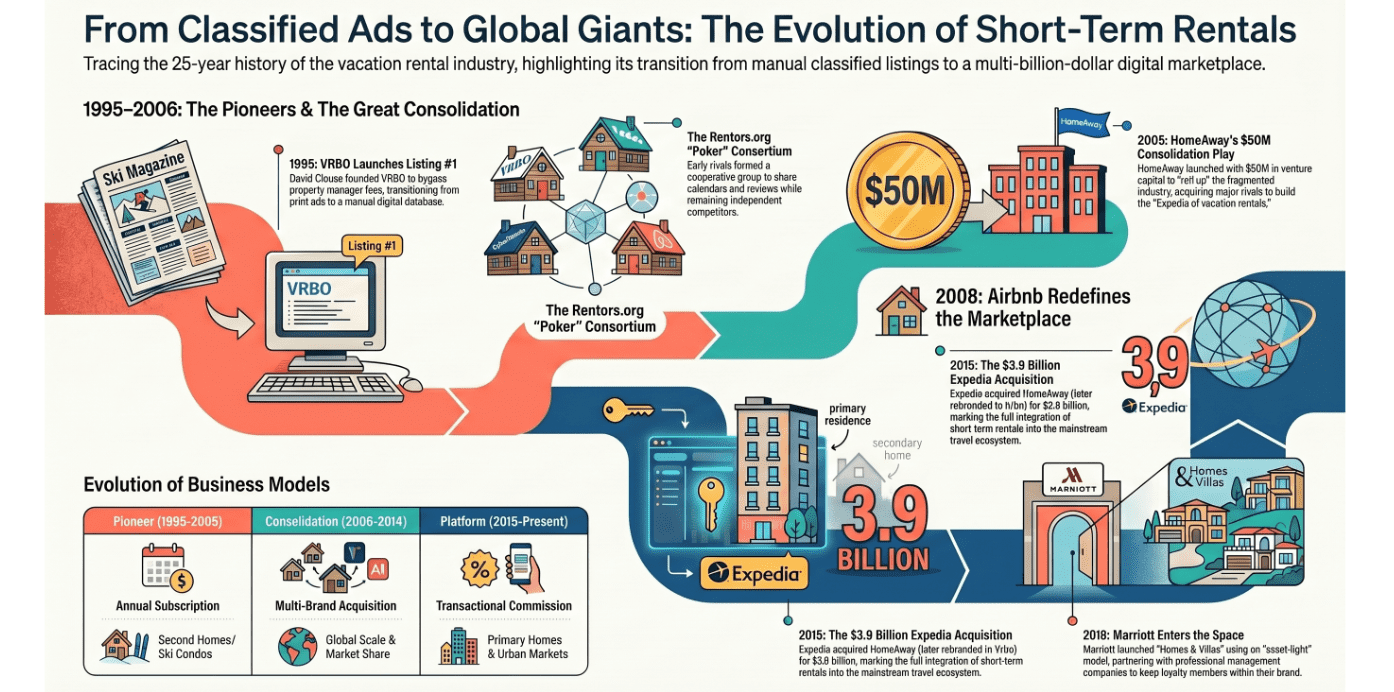

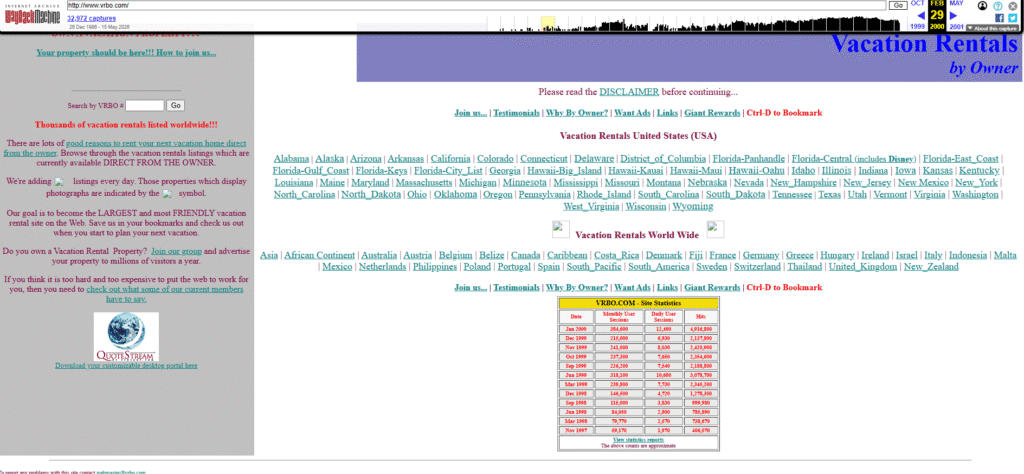

In the mid-1990s, the vacation rental sector was highly fragmented, a collection of “lifestyle businesses” that operated as a digital mirror of newspaper classifieds. Strategically, the transition to the internet was not a move toward modern e-commerce, but a “subscription-only” foundational bridge. This model allowed property owners to migrate from the static pages of print media to the rudimentary web without surrendering their status as the sole merchant of record. It was a digital evolution that preserved the owner’s sovereignty while extending their reach beyond the local “drive-to” markets.

The business philosophy of David Clouse (VRBO) and the CyberRentals founders was rooted in disintermediation. Clouse, a computer programmer, viewed the internet through a diagnostic lens: as a tool to “weasel out” high commissions charged by traditional property managers (sound familiar?).

These early pioneers viewed their platforms as lead-generation engines rather than transactional marketplaces. Owners remained responsible for the entire value chain, including vetting guests by phone, processing credit cards manually, and managing on-site logistics. Growth was throttled by high operational friction; for years, the primary “technology” involved scanning paper photos mailed by owners and manually transposing database entries into HTML.

The Early Pioneer Model: Benefits and Limitations

| Feature | Strategic Intent | Impact on Scale |

| Annual Subscription Fee | Low-barrier entry ($72–129/year) specifically designed to bypass the 45% commissions of property managers. | Rapidly aggregated thousands of “Rent-by-Owner” listings via bootstrap growth. |

| Manual Data Onboarding | “Scanning paper photos” mailed by owners to maintain baseline visual quality. | Significant operational friction; scaling was limited by the speed of manual labor. |

| Owner as Merchant | Maintain owner control over guest vetting and the “merchant of record” status. | Preserved “host sovereignty” but created a fragmented, opaque, and inconsistent guest experience. |

| Organic SEO Focus | Keyword stuffing and short URLs (vrbo.com) to capture search intent before Google’s dominance. | Established massive “First-Mover Advantage” and high-intent traffic without marketing spend. |

As the landscape matured, the Rentors.org (now redirects to VRBO) consortium emerged as a critical defensive precursor to consolidation. This early horizontal integration allowed competitors to share calendars and reviews, ensuring that fragmented owners didn’t have to manually update multiple sites. This cooperation provided the “listing layer” necessary to sustain the industry before the era of massive corporate aggregation began.

2. Aggregation as a Precursor to Transaction

The 2004–2006 period marked a definitive shift toward professionalisation, driven by the strategic insight that in a marketplace business, market share through acquisition is the ultimate lever. HomeAway founders Brian Sharples and Carl Shepherd realised that the “Winner-Take-All” logic of digital platforms required immediate scale. Conversely, early Expedia innovators like Rich Barton suffered from “Tech Snob” arrogance; they focused on building sophisticated reservation software for a supply side that was not yet technologically literate. This strategic myopia allowed HomeAway to bootstrap a global empire by acquiring the “kludgy,” cash-generative classified sites that the tech giants dismissed as unprofessional.

These are examples of the fees charged in the US and Europe that property owner and managers had based their business models on:

- UK: OwnersDirect in 2000: 12 Months + 3 Months Free :- £100

- UK: Holiday Lettings (2002): Direct service (£25 per annum): (Acquired by TripAdvisor)

- USA: VRBO (2000): A full one-year membership is available for $108 US.

- DE: Few-direkt.de 2000: from 29 DM ($11) per month

- FE: Abritel 2000: 490 FF for 1 year

As we can see, charging £100 or $150 per property or a lot less was the norm. All data is available from archive.org, the Wayback Machine

The centrepiece of this consolidation was the 2006 acquisition of VRBO. David Clouse, operating from a non-negotiable price point, sold for an estimated 130–160 million. The acquisition presented a unique forensic accounting challenge: HomeAway had to transform a company where employees were members of the Church of the Nazarene and operated out of basements into a GAAP-compliant public entity. Furthermore, the business was structured across multiple LLCs in the U.S. Virgin Islands as a tax-mitigation strategy. The strategic urgency of the deal was underscored by competitive tension; Expedia attempted a late-stage “Thursday call” to intercept the deal, but the announcement was already slated for Friday, cementing HomeAway’s dominance.

This is now big business!

During this era, HomeAway utilised a “Shelf Space Strategy,” maintaining separate brands like GreatRentals, CyberRentals, and A1 to dominate Google organic search. By controlling the top five search results for high-value keywords, HomeAway captured 99% of the industry’s traffic. However, this created a “Platform Dependency Trap.” As Google’s algorithms evolved to penalise duplicate content, HomeAway was forced into a costly and complex technical integration to move from a multi-brand fleet to a unified platform. This consolidation of secondary-home listings professionalised the supply side but left the market vulnerable to total category disruption.

3. The Airbnb Disruption: Primary Homes and the Frictionless Model

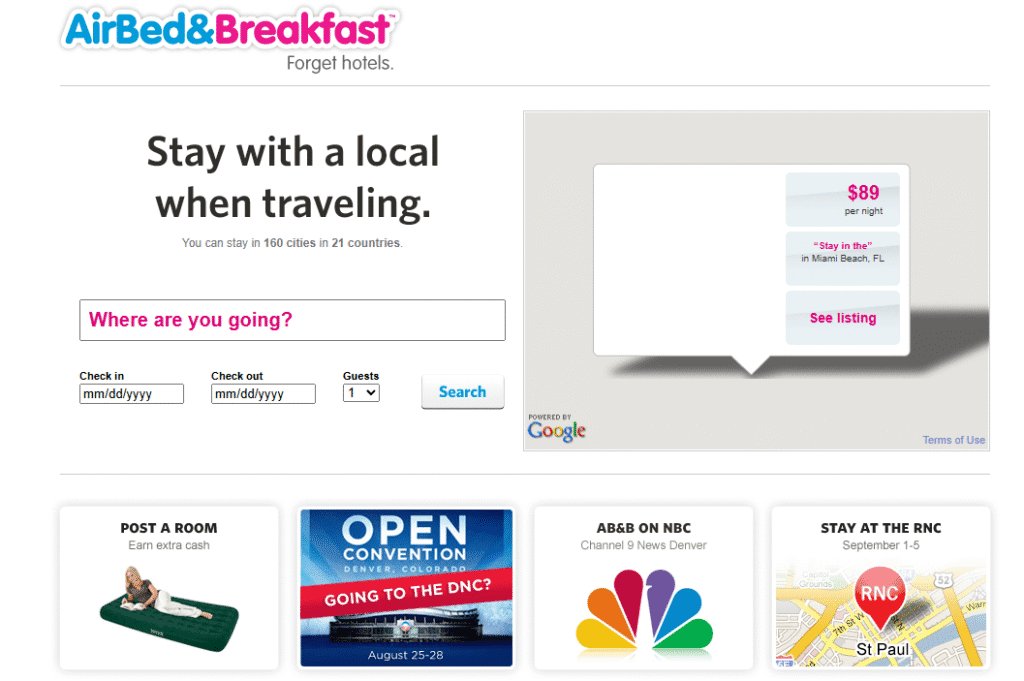

The 2007 arrival of Airbnb marked a radical departure from the subscription model by creating the “primary home” rental category. While HomeAway was focused on the asset-heavy secondary-home market, Airbnb utilised “First-Mover Regulatory Arbitrage” to unlock a massive, untapped supply of urban apartments. By operating in a legal grey area, effectively “thumbing their noses” at antiquated regulations in cities like New York and Paris, Airbnb bypassed the compliance hurdles that publicly traded entities like Expedia initially feared. Despite recent moves, the hotel market was the target too.

Airbnb’s “Transactional” philosophy triggered a fundamental erosion of host sovereignty in favour of platform-led guest assurance. By controlling payment flows and the user experience, Airbnb addressed the trust deficit plaguing the subscription model. In the old VRBO paradigm, guests mailed checks and “blindly trusted” owners (which worked fine before cybercriminals); Airbnb replaced this with a robust “Trust Layer.” This strategic moat moved the industry from the fringes of “couch surfing” to a legitimate, mainstream lodging powerhouse.

The Two Pillars of the Airbnb Trust Layer and how OTAs succeeded.

- Integrated Payments: The platform became the merchant of record, removing the friction of manual checks and ensuring secure payouts.

- Two-Way Social Proof: A reputation-based marketplace where verified reviews for both guests and hosts mitigated the inherent risk of the “primary home” model.

This shift to a frictionless, transactional model fundamentally changed the power dynamic: the platform now dictated the terms of the stay, shifting the industry toward a hospitality-standard experience.

4. The Professionalisation Conflict: Software Wars and Tensions

As the industry moved toward a unified transactional model, the “Software Layer” became the new battlefield. HomeAway’s acquisition of property management (PM) software firms in 2010 (e.g Escapia) a move to control the “pipes” of inventory. By owning the tools used by professional managers, HomeAway could enforce “push-button access,” effectively forcing a fragmented market to professionalise and synchronise. This move sparked significant friction between platforms and suppliers, as property managers feared the “disintermediation” of their data.

Value Proposition Shifts for Property Managers

- Take-Rate Compression: The traditional high commission fee was challenged by tech-enabled, lower-fee models from firms like Evolve and Vacasa, which utilised asset-light scaling.

- Operational Automation: Transitioning from manual “closed-door” inspections to tablet-based virtual inspections and automated housekeeping management.

- Yield Management & Global Distribution: Moving from local Seasonal only” to year-round global exposure through OTAs, leveraging data-driven dynamic pricing.

This era bridged the gap between individual hosts and professional conglomerates, signalling the end of the “lifestyle business” and the rise of the lodging manager as a data-driven operator.

Before the final move to transactional monetisation, HomeAway introduced substantial subscription changes, colloquially known as the “Metallics” by operators, which were met with substantial hostility. Our own records show that fees tripled for the same booking exposure as the industry accelerated.

Tier Approx Annual Cost (USD)

Classic $299–$349 ~£199–£249

Bronze $499–$699 ~£350–£500

Silver $799–$1,200 ~£600–£900

Gold $1,500–$2,500 ~£1,200–£2,000

Platinum $3,000–$8,000+ ~£2,500–£6,000+

5. The Final Pivot: From Subscription to Transactional

By 2015, the “Subscription” model had become a strategic liability for HomeAway/Vrbo. The success of Airbnb’s commission-based model and the subsequent $3.9 billion acquisition of HomeAway by Expedia forced an “Ugly Transition.” Forcing a move from predictable subscription revenue to a commission-based model while under public investor scrutiny was a high-risk manoeuvre. It required migrating hundreds of millions in revenue while facing massive host churn and internal friction.

The COVID-19 pandemic served as the ultimate litmus test for these models. When the crisis hit, Airbnb unilaterally enforced a guest-centric refund policy, which, while protecting travellers, left many hosts feeling betrayed and facing bankruptcy. Vrbo attempted a more balanced approach, allowing owners and travellers to negotiate, which the CEO noted led to high-stakes volatility, including literal death threats from travellers over refund disputes. This divergence redefined “Host Love”; Vrbo capitalised on Airbnb hosts’ betrayal by launching the “Fast Start” program to recruit disaffected supply.

The Current Competing Visions for the Future of Lodging

- The “Connected Trip” (Booking.com/Expedia): A focus on utility, scale, and seamlessness. This vision aims to tie together flights, cars, and homes into a single, automated point of contact, treating short-term rentals as commoditised rooms in a global lodging engine.

- The “Lifestyle Curator” (Airbnb): A focus on community and inspiration. Drawing parallels to Netflix, this vision uses data to curate “magical” experiences and vegetarian itineraries, positioning the platform as a holistic lifestyle brand rather than a mere booking site.

Over 25 years, the industry has undergone a total strategic metamorphosis, evolving from one “stupid four-letter name” in a Colorado basement and a collection of disparate European enquiry sites into a multi-billion dollar global lodging powerhouse that has fundamentally rewritten the rules of hospitality, and now dominated by Airbnb in the specific STR sector and Booking.com a close second.

An Alternative Vision

The Path Forward: Direct Bookings, AI, and Subscriptions. The sources agree that relying on OTAs for the vast majority of your business is a fragile strategy, and there is immense economic incentive to dilute their power.

- Direct Bookings: Even converting just 50% of your bookings away from OTAs to direct channels can be transformative, potentially returning massive margin to your bottom line.

- Leveraging AI: Historically, OTAs won because independent websites couldn’t compete with their technology, SEO, and user experience. However, AI is actively flattening these advantages. Modern AI-driven tools—such as AI website builders, automated SEO, conversational booking interfaces, and intelligent CRM systems—are drastically lowering the barriers to efficiently capturing direct bookings.

- The Return of Subscriptions: As OTA fees escalate, the math behind subscription sites makes sense again. If an annual subscription costs $500, securing just one peak-season booking through that channel can more than offset the cost of OTA commissions. Furthermore, these channels allow you to own the guest relationship, retain customer data, and build your own brand footprint.

The industry’s most successful future operators will likely be those who actively reduce their OTA dependency below 50% and use AI aggressively to regain control over their margins and guest relationships.

Will AI level the playing field, or just give OTAs more power?

Would you like to explore the specific AI tools and strategies mentioned in the sources that can help you increase direct bookings and operational efficiency? That’s our next focus! Stay tuned!