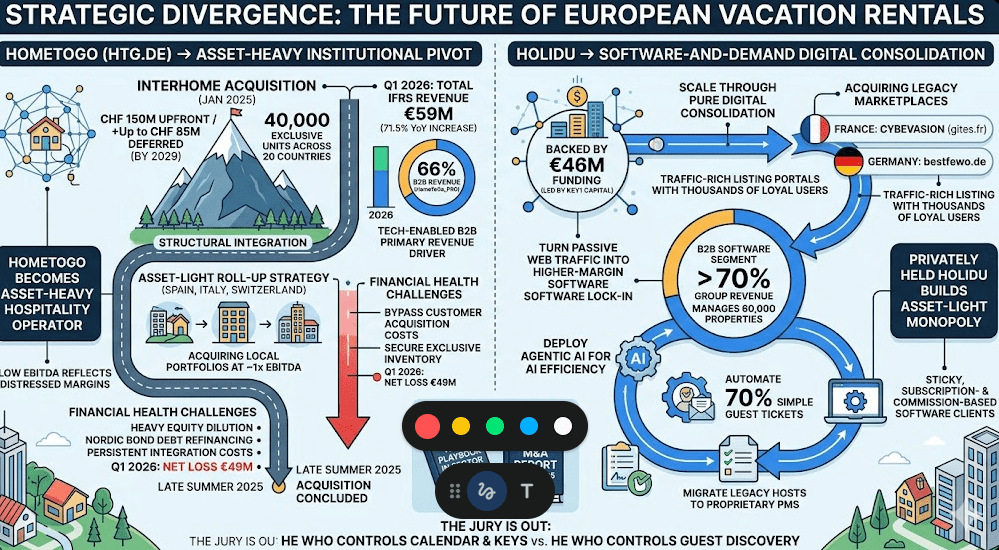

It appears HomeToGo has made an aggressive operational pivot toward a business-to-business model, relying heavily on its acquisition of Interhome from the Swiss retail conglomerate Migros, a transformative deal valued at a CHF 150 million upfront purchase price, plus up to CHF 85 million in deferred payments through 2029.

We have been curious about the success of listing platforms and meta-search engine businesses for a while now in light of Booking, Expedia and Airbnb’s market dominance, and hence a quick look at their results and Holidu below.

Interhome Acquisition Benefits

By absorbing Interhome’s large footprint of approximately 40,000 exclusively managed vacation rentals across 20 countries, the platform has fundamentally shifted its core architecture. This structural integration drove a 71.5% year-over-year surge in total Group IFRS revenue to €59 million in Q1 2026, positioning the tech-enabled B2B segment, HomeToGo_PRO, as the firm’s primary revenue and profit driver, accounting for 66% of total group turnover.

To optimise this capital-intensive ecosystem, HomeToGo seems to be executing a hyper-localised, asset-light roll-up strategy, buying out small regional competitor portfolios across Spain, Italy, and Switzerland at a compressed ~1x EBITDA multiple.

This exceptionally low multiple probably reflects the distressed operating margins of fragmented, independent operators unable to scale or fund digital transformation, enabling HomeToGo to bypass traditional customer-acquisition costs and efficiently secure exclusive, high-quality inventory.

However, while this buy-and-build strategy provides immediate valuation arbitrage and masks completely flat organic growth in the legacy B2C marketplace, the broader financial health remains under acute pressure; heavy equity dilution, substantial debt refinancing via Nordic bonds, and persistent integration costs have widened statutory net losses to €49 million.

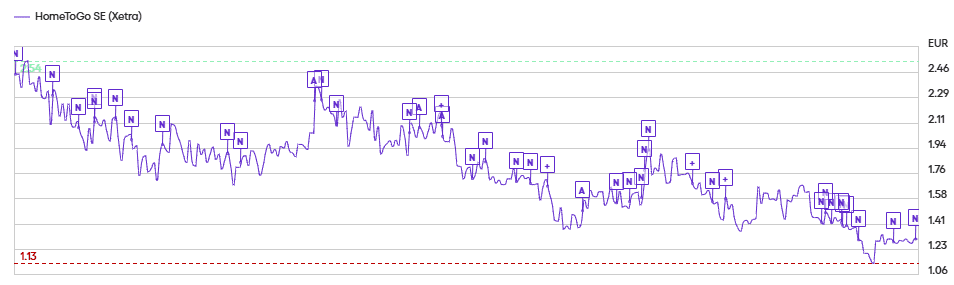

Its share price has not moved dramatically. The Interhome acquisition was announced in January 2025 and concluded in late summer.

Acquiring at Scale to increase growth is an opportunity, but it will require substantially larger deal sizes or substantial investment in organic growth.

Also note that Hometogo owns the PMS company Smoobu, which is also a feeder of inventory, but operates in a highly competitive market.

OUR M&A REPORTS

Please see our a) M&A playbook for M&A in this sector, our 2025 M&A report, and our own involvement in M&A deals over the last 12 months, which have seen companies moving at between 2.5 and x 5 times EBITDA.

What about Holidu?

While its cross-town rival HomeToGo has chosen an asset-heavy, institutional path by acquiring Interhome’s physical operations, Holidu is executing a software-and-demand strategy.

Backed by a further €46 million funding round led by Key1 Capital, Holidu has chosen to scale through pure digital consolidation rather than taking on the messy logistics of linen and keys. By acquiring legacy consumer marketplaces, such as France’s dominant portal Cybevasion (gites.fr) and Germany’s bestfewo.de, Holidu is quietly cornering the fragmented, independent host market. This aligns with HomeAway’s old roll-up strategy and also follows up on Spain-Holiday.com acquisiiton and merger with the Holidu subsidiary Bookiply in 2021.

The Holidu playbook lies in turning passive web traffic into higher-margin software lock-in. Instead of competing on the expensive Google Ads battlefield for customer acquisition, Holidu buys localised, traffic-rich listing portals that already possess thousands of loyal users. They then migrate these legacy, “request-to-book” hosts onto their own proprietary Property Management Software (PMS).

This tactical conversion turns non-technical private homeowners into sticky, subscription- and commission-based software clients. Today, Holidu’s B2B software segment accounts for over 70% of the group’s total revenue and manages a unified portfolio of nearly 60,000 properties. By avoiding the operational overhead of physical property management, Holidu is uniquely positioned to maximise AI efficiency. While HomeToGo must deploy capital into real-world logistics, Holidu is leveraging “agentic” AI to scale its customer support, already automating 70% of simple guest tickets via software agents. Some may consider that as HomeToGo risks becoming a traditional, debt-laden hospitality operator under public-market scrutiny, privately held Holidu is quietly building an agile, asset-light monopoly over the independent European host.

The jury is out, as there are successful models of each! He who controls the calendar and keys, and he who controls the guest discovery and brand loyalty.